How the mid-market is future-proofing growth

Scaling sustainability

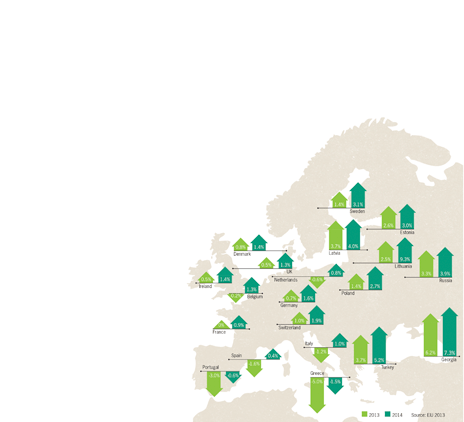

Grant Thornton’s 2025 Sustainability Report reveals how mid-market businesses worldwide are driving growth through sustainability. Explore key insights, statistics, and global trends shaping the future of responsible business.

|

21 Oct 2025